2 min leer

La Pregunta del Billón de Dólares: ¿Está el Auge de la IA basado en Acuerdos Circulares o en una Demanda Real?

Categoría

El mundo de la IA

Compartir artículo

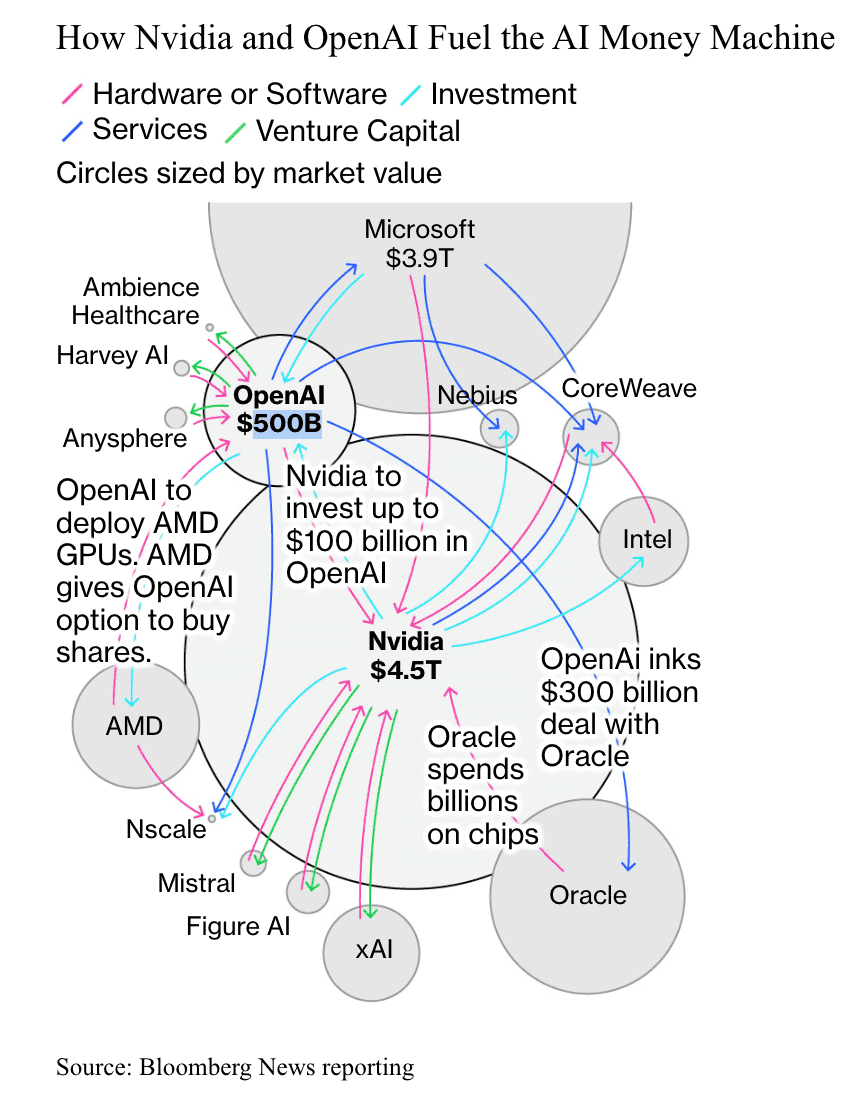

La carrera por liderar el futuro de la inteligencia artificial ya no se mide en algoritmos, sino en gigavatios. En los últimos meses, OpenAI ha anunciado varias alianzas de infraestructura a gran escala con Nvidia, AMD, Broadcom y Oracle, que en conjunto podrían redefinir la evolución de la economía del procesamiento de datos a nivel global.

Bloomberg describió recientemente estos acuerdos como “alianzas circulares”, en las que proveedores, inversores y clientes quedan interconectados en bucles de capital y capacidad. La cifra principal es asombrosa: aproximadamente 1 billón de dólares en compromisos superpuestos que podrían redefinir la cadena de suministro de la IA. Sin embargo, a medida que aumenta la expectación, también lo hace el escepticismo sobre la sostenibilidad real de estos modelos.

Las cifras detrás de la fiebre por la infraestructura de IA

La estrategia de OpenAI para expandir su capacidad de procesamiento abarca ahora múltiples proveedores y tecnologías.

Nvidia firmó una declaración de intenciones por 10 gigavatios de sistemas de IA, y la compañía planea invertir hasta 100.000 millones de dólares para llevar a cabo estos despliegues, según Reuters.

AMD le siguió con un acuerdo de 6 gigavatios para sus GPU Instinct de última generación, confirmado en un comunicado oficial de AMD. Algunos medios, como Tom's Hardware, han informado de que el acuerdo podría incluir una opción de compra para que OpenAI adquiera hasta el 10% de las acciones de AMD, aunque la propia AMD no lo ha confirmado.

Para diversificar aún más, Broadcom co-diseñará aceleradores personalizados con OpenAI, con el objetivo de ofrecer alrededor de 10 gigavatios de rendimiento para 2029, según Reuters.

Por último, se informa que Oracle ha asegurado un contrato de alojamiento en la nube de 300.000 millones de dólares a lo largo de varios años para respaldar los planes de escalabilidad de OpenAI (The Wall Street Journal).

Cada una de estas alianzas responde a un propósito estratégico. Juntas, crean una red de dependencias, y es precisamente ahí donde surge la preocupación por el carácter “circular” de este modelo.

Qué significan realmente los acuerdos circulares

Un acuerdo circular ocurre cuando el mismo dinero y capacidad se mueven a través de socios interconectados. Una empresa financia la expansión de otra, que luego utiliza ese dinero para comprar los productos de la primera compañía.

In AI, estos ciclos pueden incluir participaciones de capital, líneas de crédito o «respaldos de capacidad», donde los proveedores se comprometen a comprar inventario no vendido entre sí. Un ejemplo muy conocido es el acuerdo de CoreWeave y Nvidia, en el cual Nvidia supuestamente tiene acceso a capacidad de GPU no utilizada en los centros de datos de CoreWeave, garantizando de manera efectiva la utilización incluso si la demanda se debilita (Financial Times).

Los acuerdos circulares no son intrínsecamente malos. Pueden alinear incentivos y facilitar la financiación de grandes proyectos. Pero si demasiado crecimiento depende de estos bucles internos, la demanda del mundo real puede estar sobredimensionada.

Por qué todo el mundo está jugando al mismo juego

El auge de la IA ha empujado a todos los actores a asegurar la mayor cantidad de capacidad de cómputo posible. Las cadenas de suministro de chips avanzados siguen estando limitadas, por lo que los grandes compradores como OpenAI, Anthropic y Meta están firmando contratos a largo plazo para asegurar capacidad con años de antelación.

La estrategia de diversificación de OpenAI tiene sentido sobre el papel. Nvidia sigue siendo el proveedor dominante, pero la competencia se está intensificando. Las GPU Instinct de AMD y los chips personalizados de Broadcom ofrecen alternativas que podrían reducir costes y mejorar la eficiencia. Al distribuir los pedidos, OpenAI reduce el riesgo, gana poder de negociación en los precios y garantiza la redundancia.

Para los proveedores, estos acuerdos son irresistibles. Garantizan flujos de ingresos durante años y atraen la confianza de los inversores. Las acciones de AMD, por ejemplo, subieron con fuerza tras su anuncio con OpenAI, y la capitalización de mercado de Broadcom alcanzó máximos históricos tras las noticias de su alianza para chips personalizados.

El resultado es un bucle de retroalimentación: los laboratorios de IA compran chips para entrenar modelos más grandes, los fabricantes de chips expanden sus fábricas para satisfacer esa demanda, y los mercados de capitales recompensan a todos los implicados. Pero, como han advertido los analistas, estos bucles pueden amplificar tanto el crecimiento como la fragilidad.

Dónde comienzan los riesgos

1. Demanda sobredimensionada

Si la adopción de la IA en empresas y consumidores se ralentiza, la enorme capacidad que está entrando en servicio puede superar el uso real. Con unos costes de construcción y equipamiento de centros de datos de aproximadamente 50.000 millones de dólares por gigavatio (Financial Times), incluso una pequeña brecha entre la oferta y la demanda puede generar una enorme tensión financiera.

2. Financiación de proveedores y exposición oculta

Cuando los proveedores ayudan a financiar a sus propios clientes, o toman participación en ellos, la línea entre inversión y ventas se difumina. Los ingresos reportados pueden aumentar, pero el flujo de caja subyacente podría seguir siendo débil. Analistas de Morgan Stanley y Morningstar han señalado este problema como un indicio de riesgo de «financiación circular» en el mercado actual de la IA.

3. Respaldos contractuales

Muchos contratos de infraestructura incluyen cláusulas de tipo «take-or-pay» (paga o asume), lo que significa que los compradores deben pagar por la capacidad tanto si la utilizan como si no. Estos respaldos mantienen alta la utilización, pero pueden comprometer la liquidez si la demanda de IA disminuye.

4. Transparencia limitada

Las empresas rara vez revelan qué parte de su cartera de pedidos o de sus ingresos declarados proviene de partes vinculadas. Sin ese detalle, los inversores no pueden determinar hasta qué punto el crecimiento depende de la financiación interna.

Sólidos motivos para el optimismo

Para ser justos, no toda esta inversión es especulativa. Existen razones estructurales de peso para creer que la infraestructura de IA tendrá una gran demanda durante la próxima década.

Personalización del hardware

Al colaborar con Broadcom para diseñar sus propios chips, OpenAI sigue un camino iniciado por las Unidades de Procesamiento de Tensor (TPU) de Google. El silicio personalizado y adaptado a modelos específicos puede mejorar drásticamente el rendimiento por vatio, reduciendo los costes operativos a largo plazo.

Resiliencia de múltiples proveedores

Depender exclusivamente de Nvidia expone a cualquier empresa de IA a cuellos de botella en el suministro y al poder de fijación de precios de un solo actor. Las alianzas con AMD y Broadcom no solo amplían la oferta, sino que fomentan una innovación más rápida en todo el ecosistema.

Retorno a largo plazo

El entrenamiento de modelos de frontera como GPT-5 y GPT-6 requiere exponencialmente más capacidad de cómputo. Si la IA continúa integrándose en los flujos de trabajo empresariales, las búsquedas en tiempo real y la robótica, el actual ritmo de construcción de infraestructuras se considerará una preparación temprana en lugar de un exceso.

Incluso el CEO de Nvidia, Jensen Huang, argumentó recientemente que la economía de la IA está impulsada por una demanda real y no por el hype, señalando que todas las industrias clave ya están integrando la IA en sus procesos de producción e interfaces de cliente (Windows Central).

Aspectos clave a seguir de cerca

Si desea distinguir la expectación del progreso real, monitorice las siguientes señales durante los próximos 12 a 18 meses:

Tasas de utilización de grandes clústeres de GPU

Crecimiento de ingresos frente al gasto de capital (CapEx) en fabricantes de chips y laboratorios de IA

Desglose de transacciones con partes vinculadas en los informes financieros trimestrales

Restricciones de energía y suministro eléctrico en la construcción de centros de datos

Métricas reales de adopción empresarial (contribución de los ingresos de IA por sectores)

Si la utilización y los ingresos aumentan en sintonía con el crecimiento de la infraestructura, la etiqueta de economía circular podría resultar excesivamente cautelosa. De lo contrario, podríamos enfrentarnos a una corrección similar a la que experimentó el sector de las telecomunicaciones a principios de la década de 2000.

En conclusión

La carrera por la infraestructura de IA es tanto un hito como una advertencia. Refleja una coordinación sin precedentes entre fabricantes de hardware, desarrolladores de modelos y proveedores de nube, pero también introduce un nivel de complejidad financiera raramente visto fuera de las burbujas especulativas.

Los acuerdos circulares han permitido que el sector avance a una velocidad vertiginosa, asegurando la disponibilidad de cómputo y acelerando los ciclos de producto. Sin embargo, también significan que parte de este engranaje de un billón de dólares depende de que el dinero fluya de forma circular.

La prueba de fuego llegará cuando la demanda externa —procedente de empresas, administraciones públicas y consumidores— tenga que justificar todo el capital ya invertido. Si las herramientas de IA aportan un valor transformador a las distintas industrias, el bucle se sostendrá. Si no, algunos de esos círculos podrían empezar a romperse.

Y para las empresas que desarrollan aplicaciones prácticas de IA en lugar de infraestructuras a hiperescala, la lección es evidente: la agilidad importa más que el exceso. Plataformas como Beam AI están demostrando que la automatización inteligente no requiere una capacidad multimillonaria, sino un despliegue más inteligente del cómputo que ya tenemos a nuestra disposición.