6 دقيقة قراءة

Why Insurance Companies Are Replacing Rules Engines With AI Agents in 2026

Category

أتمتة العملاء

Share the article

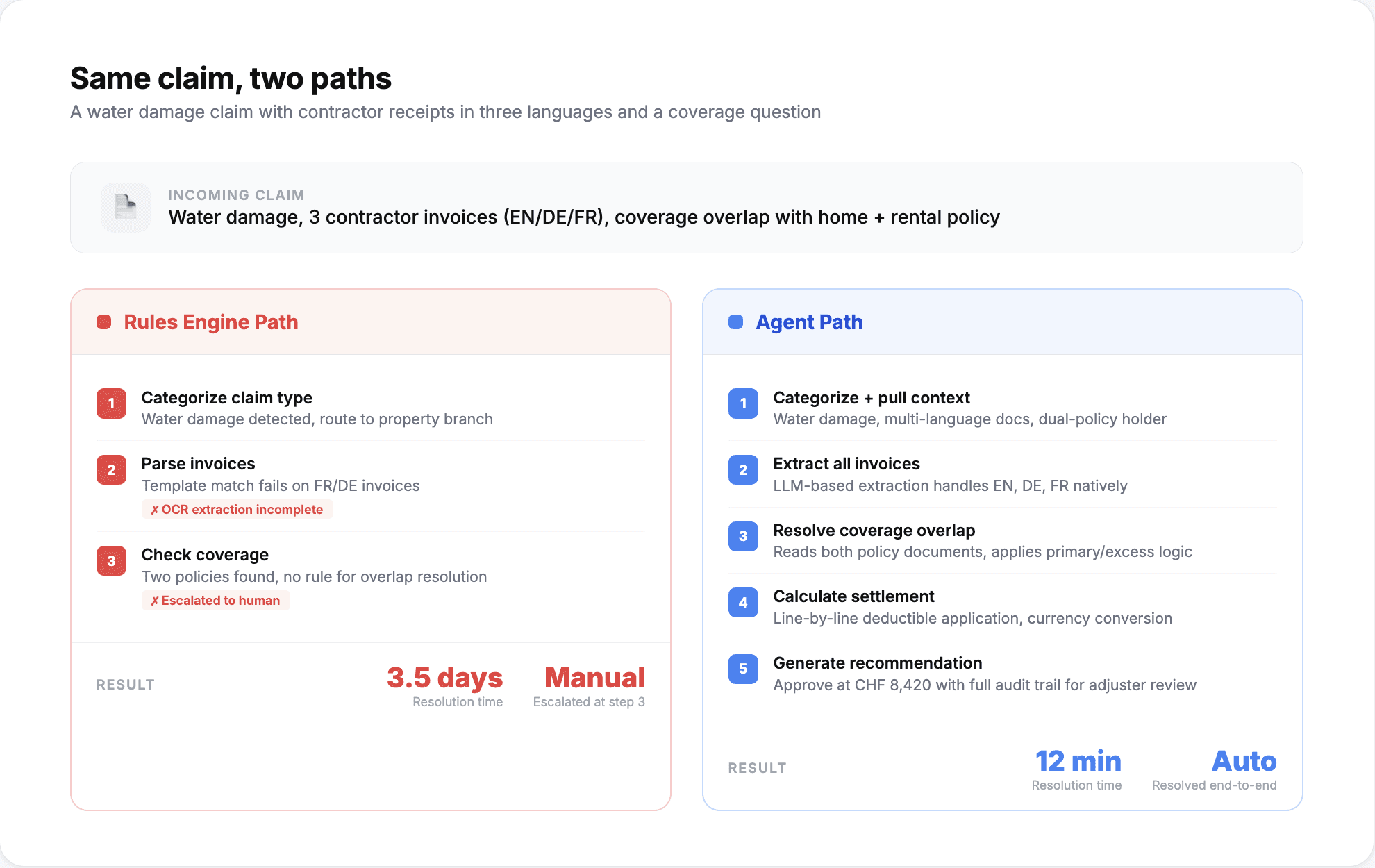

Rules engines were supposed to solve insurance automation. Define the conditions, map the outcomes, deploy the decision tree, and let the system handle claims without human intervention. For simple, high-volume decisions like checking whether a policy is active, they work fine.

The problem shows up when claims get even slightly complex. A rules engine for motor claims might have 200 conditions covering standard scenarios. But a customer submits a claim involving a rental car in a different country, partial liability, and a pre-existing damage dispute. The rules engine either rejects it outright or flags it for manual review. An insurer running 50,000 claims per month might automate 30-40% through rules. The other 60-70% still lands on an adjuster's desk, often with no context about why the system could not handle it.

This is the gap that AI agents are filling. Not by replacing the rules engine entirely, but by handling the middle tier of claims that are too complex for static rules and too routine for senior adjusters. One European insurer automated 91% of motor claims decisions after deploying AI agents alongside their existing rules engine. Processing speed increased 46% and customer satisfaction scores rose 9%.

What rules engines cannot do (and were never designed to)

Rules engines execute pre-defined logic. That is both their strength and their ceiling.

They cannot interpret unstructured data. A claims adjuster reading a police report, a repair estimate, and three photos of vehicle damage is doing something fundamentally different from matching fields in a database. They are extracting relevant facts from messy, inconsistent documents, weighing their reliability, and forming a judgment. Rules engines need structured inputs. Anything that arrives as a PDF, an image, or free-form text requires a human to convert it into fields the engine can process.

They cannot handle exceptions they were not programmed for. Every new edge case requires a developer to add a new rule. Over time, this creates massive rule sets where the interactions between rules become unpredictable. Insurance IT teams commonly manage rules engines with 500-1,000+ conditions, and changing one rule can cascade into unexpected outcomes in others. A McKinsey analysis of insurance operations found that rule complexity is the primary reason automation rates plateau at 30-40% for most carriers.

They do not learn from outcomes. If a rules engine approves a claim that turns out to be fraudulent, or flags a legitimate claim that wastes three days of adjuster time, nothing changes in the system. The same error will repeat until someone manually identifies the pattern and writes a new rule. By then, the damage, both financial and to customer experience, has already compounded.

How AI agents handle what rules engines cannot

AI agents for insurance claims work differently from rules engines in three specific ways.

They process unstructured documents directly. An agent ingests the claim submission, including photos, PDFs, free-text descriptions, and third-party reports, and extracts the relevant data points without requiring manual conversion. A US agribusiness insurance deployment uses agents to process 15,000 data points monthly across weather reports, satellite imagery, and historical yield data, achieving 93% automation in data aggregation with 85% faster underwriting decisions.

They apply contextual reasoning, not just pattern matching. When an agent evaluates a claim, it considers the policy terms, the claim history of the policyholder, similar claims from the past 12 months, and the specific details of the incident. This is closer to how a mid-level adjuster thinks than how a decision tree executes. The agent can determine that a $2,400 repair claim on a vehicle with a clean history and matching documentation should be approved, while a $2,400 claim with inconsistent photos and a third repair in six months should be escalated.

They improve with feedback. When an adjuster overrides an agent's recommendation, that override feeds back into the model. Over time, the agent handles more of the gray-area claims correctly. Self-learning mechanisms) allow the system to adapt to changing fraud patterns, new policy structures, and regional claim variations without waiting for a developer to write new rules.

What 91% automation actually looks like in practice

When insurers hear "91% automation," the reasonable question is: what about the other 9%? And does automating 91% mean quality dropped?

In the European motor claims deployment, the 91% figure represents claims that agents resolved end-to-end without human intervention. The remaining 9% were escalated to adjusters, but not as cold handoffs. Each escalated claim arrived with the agent's analysis, the specific reason for escalation, and a recommended action. Adjusters were reviewing a prepared brief, not starting from scratch.

The quality data tells the rest of the story: customer satisfaction (NPS) increased 9% after deployment. Claims that previously took 60 days to resolve were closing in three. Adjusters who previously handled 40-50 routine claims per day shifted to handling 15-20 complex claims with significantly more context and time per case.

For the US agribusiness insurer, the impact was similar but in a different dimension. Underwriting speed, not claims processing, was the bottleneck. Agents automated 93% of the data aggregation that underwriters previously did manually, pulling from weather databases, USDA crop reports, and satellite providers. Underwriting decisions that took a week now take a day, and the accuracy of risk assessments improved because agents process more data points than a human underwriter can review in the same timeframe.

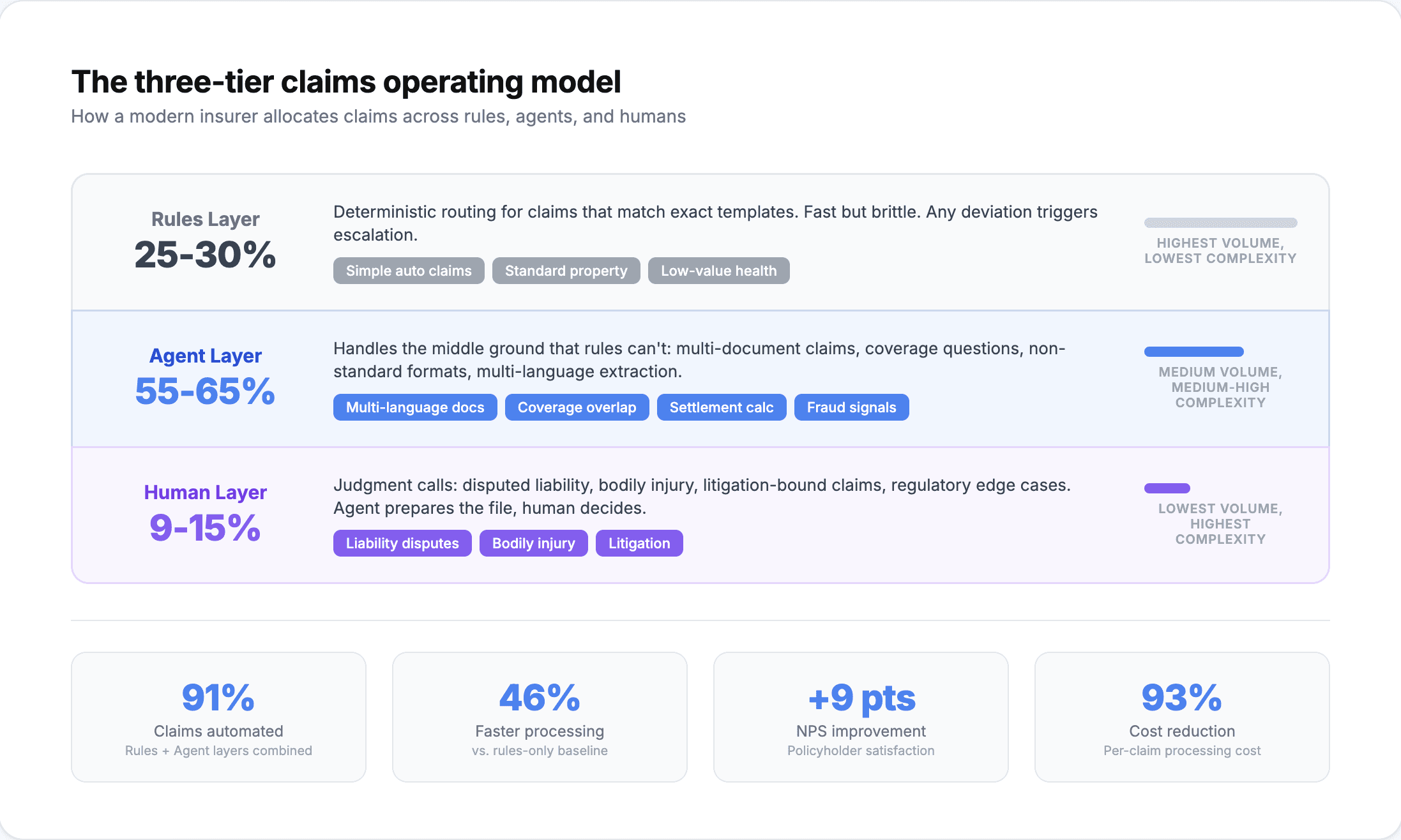

The hybrid model: agents and rules engines together

The smart deployment pattern is not ripping out the rules engine. It is layering agents on top.

Rules engines still handle the 25-30% of claims that are genuinely simple: policy verification, coverage confirmation, straightforward approvals under a threshold. These are the claims where speed matters more than judgment, and a rules engine resolves them in milliseconds.

AI agents handle the 55-65% in the middle: claims that require document interpretation, cross-referencing, or contextual judgment but follow recognizable patterns. These are the claims that currently go to adjusters by default, not because they need expert judgment but because the rules engine cannot handle the complexity.

Human adjusters focus on the 9-15% that genuinely require expertise: fraud investigations, coverage disputes, complex liability determinations, and regulatory-sensitive cases. With agents handling the middle tier, adjusters have more time and better context for the cases that actually need them.

What this means for insurance operations teams

The rules-to-agents transition is not a technology decision in isolation. It changes how claims teams are structured, how adjusters are trained, and how performance is measured.

Staffing shifts from volume to complexity. Instead of hiring adjusters to process routine claims, teams need adjusters who can handle escalations with more context and higher stakes. The role becomes more specialized, not eliminated.

Measurement shifts from throughput to accuracy. When agents handle 91% of volume, measuring adjuster productivity by claims-per-day becomes irrelevant. The metrics that matter are: escalation accuracy (are agents flagging the right claims?), override rate (how often do adjusters disagree with agent recommendations?), and resolution quality (are outcomes better or worse than the pre-agent baseline?).

Implementation is incremental, not big-bang. The insurers getting results started with one claim type, typically motor or property, proved accuracy over 90%, and expanded. Trying to deploy agents across all lines of business simultaneously is how enterprise AI projects stall.

The rules engine got insurance operations from 0% to 30% automation. AI agents are pushing that to 90%+. The carriers that move now are building the operational advantage that will be difficult to replicate once the rest of the industry follows.