7 دقيقة قراءة

AI Agents in Banking: What's Actually Working Beyond the Chatbot in 2026

Category

وكلاء الذكاء الاصطناعي

Share the article

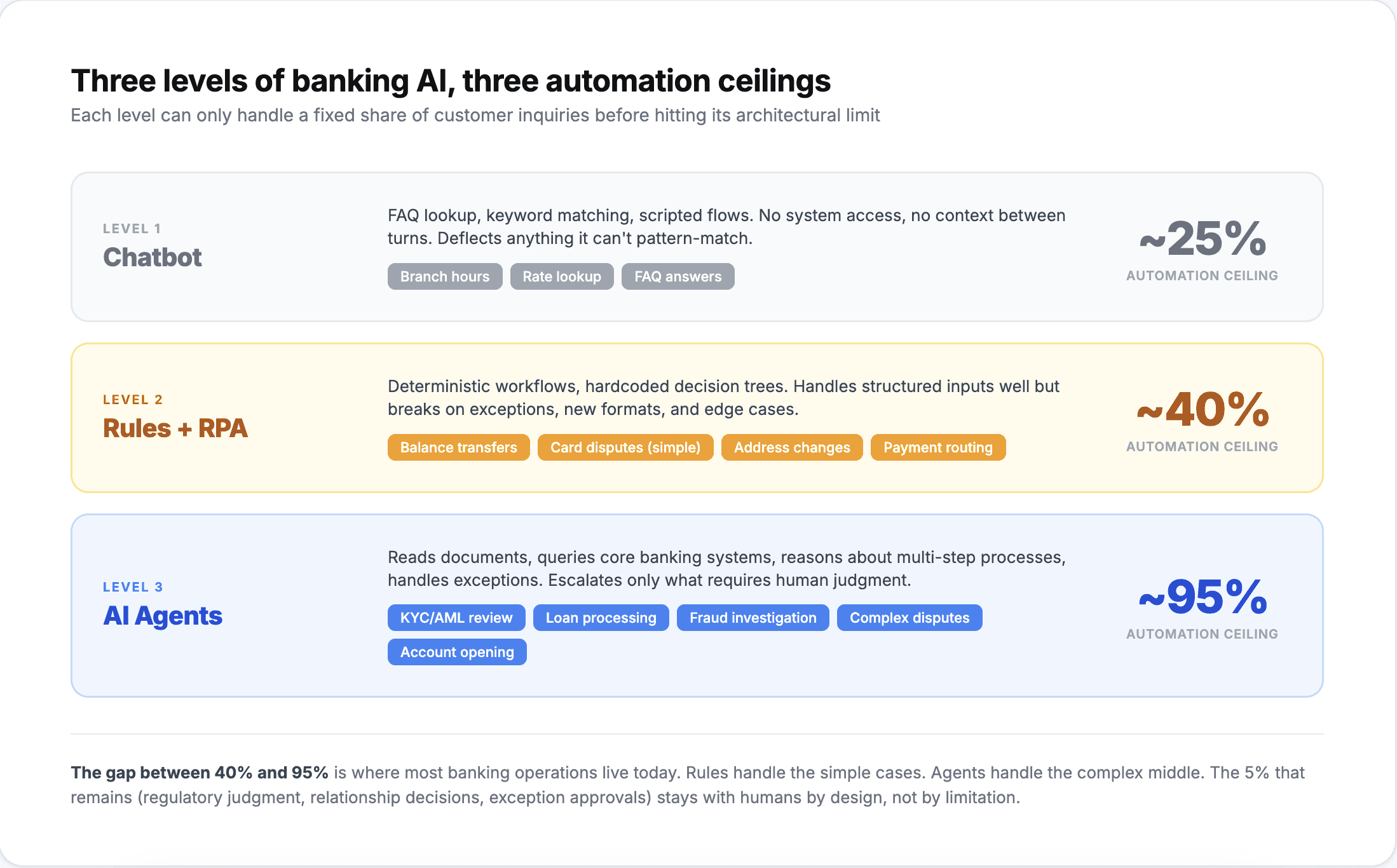

Two years ago, when a bank said "we're deploying AI," they usually meant a chatbot that answered balance inquiries and routed complaints to a human. It was a cost-saving play for the contact center, and it worked well enough for that narrow use case.

In 2026, the conversation has shifted. The banks getting measurable returns from AI are not deploying it in customer-facing channels first. They are deploying AI agents in back-office operations: KYC verification, loan document processing, transaction monitoring, and regulatory reporting. These are the workflows where manual processing is slowest, error rates are highest, and the cost of getting it wrong is measured in compliance fines, not just customer complaints.

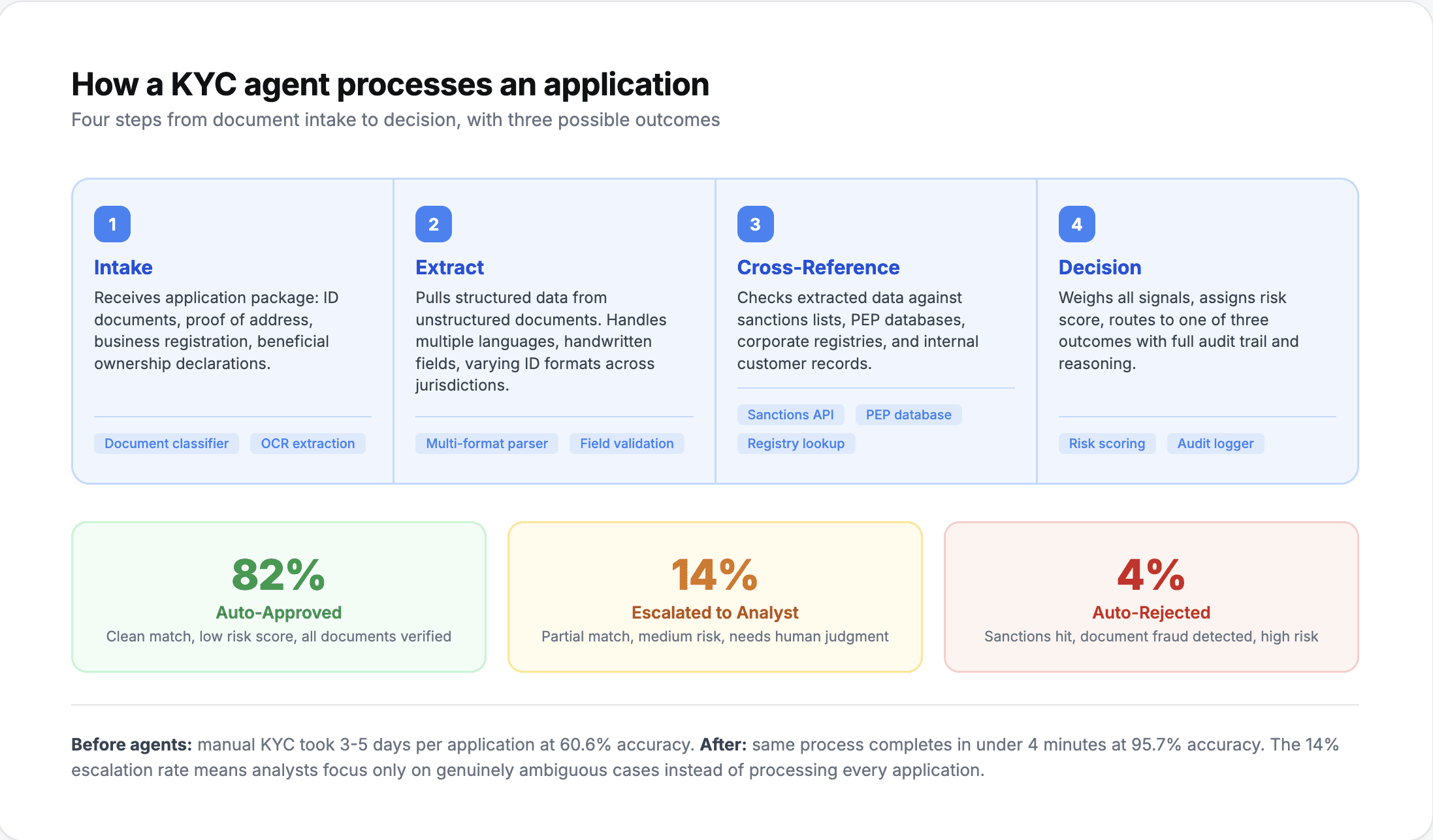

KYC and customer onboarding: from 60% to 96% accuracy

Know Your Customer verification is where most banks feel the pain of manual processes most acutely. A new customer submits an ID document, a proof of address, and sometimes a source of funds declaration. A compliance analyst verifies each document, cross-references it against sanctions lists and PEP databases, checks for inconsistencies, and makes an accept/reject decision.

The problem is accuracy at scale. A European neo-bank running manual KYC verification measured their baseline accuracy at 60.6%. Four out of ten verifications had errors: missed address discrepancies, incorrectly flagged documents, or inconsistent cross-referencing across different country formats. Not because the analysts were bad at their jobs, but because the volume of edge cases across dozens of countries, document types, and regulatory requirements made consistent accuracy almost impossible.

After deploying self-learning AI agents), that accuracy reached 95.7% within 25 minutes and three optimization cycles. The agent learned country-specific formatting rules, regulatory nuances across jurisdictions, and document variation patterns that would take a human analyst months of exposure to internalize. Onboarding times dropped because fewer applications needed manual re-review, and compliance teams could focus their attention on genuinely suspicious cases rather than routine verification errors.

The KYC use case illustrates a broader pattern in banking: the bottleneck is not decision speed, it is decision consistency across high volumes of slightly different inputs.

Loan processing: where documents meet decisions

Loan origination is a document-heavy process that has resisted automation for the same reason KYC has. The inputs are messy.

A mortgage application involves pay stubs, tax returns, bank statements, property appraisals, and employment verification letters. Each document has a different format. Some are PDFs, some are scanned images, some are digitally generated. The information across these documents needs to be extracted, cross-referenced, and validated against the bank's underwriting criteria before a loan officer can make a decision.

Traditional automation handles the structured parts: pulling credit scores, checking debt-to-income ratios against thresholds, verifying property valuations against comparable sales databases. AI agents handle the rest.

An agent processing a loan application can extract income figures from a tax return that has handwritten amendments, reconcile them against the stated income on the application, flag discrepancies between employer-provided salary letters and bank deposit patterns, and generate a summary for the underwriter that highlights what matches, what does not, and why. The underwriter gets a prepared brief with the analysis done, not a stack of documents to read from scratch.

For banks processing thousands of applications monthly, the impact compounds. Enterprise platforms processing financial operations report 98% accuracy across agent-handled workflows, with processing speeds 10x faster than manual review. A loan that previously took three days of back-and-forth between operations and underwriting can move through the document stage in hours.

Transaction monitoring and AML: reducing false positives that cost millions

Anti-money laundering transaction monitoring is the most expensive compliance function in most banks. Not because of the actual suspicious activity, but because of the false positive rate.

Industry benchmarks from the Wolfsberg Group and ACAMS put false positive rates for rules-based transaction monitoring at 95-99%. For every hundred alerts generated, only one to five represent genuinely suspicious activity. The other 95+ require an analyst to review, investigate, and dismiss. Large banks employ hundreds of analysts doing exactly this, at a cost of $50,000-80,000 per analyst per year.

AI agents reduce false positives by adding context that rules-based systems lack. Instead of flagging every transaction over $10,000 to a high-risk jurisdiction, an agent considers the customer's transaction history, the nature of their business, whether the counterparty has been verified in previous transactions, and whether the pattern matches known typologies. A wire transfer from a construction company to a materials supplier in a flagged country looks different from an identical-amount transfer from a newly opened personal account with no business documentation.

Banks deploying agents for transaction monitoring are not eliminating the compliance function. They are reducing the volume of alerts that reach human analysts by 60-80%, letting those analysts spend their time on the cases that actually require investigation. The regulatory requirement to review all alerts still applies, but the agent pre-screens and prioritizes, turning a 200-alert daily queue into a 40-alert queue where every case has context attached.

The compliance question every bank asks first

When banking teams evaluate AI agents, the first question is never "does it work?" It is "will the regulator accept it?"

This is a legitimate concern. Banking regulators in most jurisdictions require explainability for automated decisions, audit trails for every action, and the ability to demonstrate that the system is not introducing discriminatory bias. A black-box model that approves or denies loans without an audit trail is a regulatory violation waiting to happen.

AI agents deployed in banking need to meet specific compliance requirements. At minimum: GDPR compliance for data handling in European operations, SOC 2 Type II for operational security, and ISO 27001 for information security management. For banks operating in regulated US markets, HIPAA-adjacent data handling standards and OCC/FDIC supervisory guidance on model risk management (SR 11-7) also apply.

The practical answer to the regulatory question is that agents which maintain full decision audit trails, provide explainable reasoning for each action, and operate within defined policy guardrails are auditable in the same way rules engines are. The difference is that agents also improve over time, which means the audit trail includes not just what the agent decided but how its decision patterns evolved and why.

Where to start (and what to avoid)

Banks that succeed with AI agents share a common deployment pattern: they start with one high-volume, well-defined back-office workflow and expand after proving accuracy.

Best first deployment: KYC document verification. High volume, clear success criteria (accuracy rate, processing time), and well-defined regulatory requirements. Results are measurable within weeks, and the compliance team can evaluate the agent's decisions against their existing standards.

Strong second deployment: loan document processing. More complex than KYC but builds on the same document-extraction capabilities. The underwriting team provides clear feedback loops because they are already reviewing every decision.

Avoid starting with: transaction monitoring. Despite the obvious ROI from false positive reduction, AML monitoring has the highest regulatory scrutiny, the most complex edge cases, and the longest feedback loops (a suspicious activity report might not be validated for months). This is a third or fourth deployment, not a first.

The agentic platform infrastructure needed for banking deployments requires pre-built integrations with core banking systems (Temenos, Finastra, FIS), document processing capabilities, and compliance-grade audit trails. Banks running legacy core systems should confirm integration compatibility before committing to a deployment timeline. The integration layer is where most banking AI projects stall, not the agent capability itself.

The shift from automation to intelligence in banking operations

Banking has automated transactions for decades. ATMs automated cash withdrawal. Online banking automated balance inquiries. Mobile apps automated payments. Each wave automated a specific action.

AI agents automate judgment. Not the high-stakes judgment of whether to approve a $500M syndicated loan, but the routine judgment applied to thousands of daily decisions: is this document valid, does this transaction look normal, is this application complete. That routine judgment currently employs hundreds of thousands of people globally in banking operations roles.

The banks deploying agents now are not just reducing costs. They are building an operational advantage in processing speed, accuracy, and compliance consistency that compounds over time. As agents learn from each verified decision, each resolved case, and each regulatory update, the gap between agent-augmented operations and purely manual operations widens.

The question for banking operations teams is not whether AI agents work. The KYC, loan processing, and compliance data already answers that. The question is how long you continue running critical workflows at 60% accuracy when 96% is available.